CrudeQ

Turning EIA data, futures structure, volatility, and positioning into analyst-grade weekly market intelligence.

The Platform

Built to simulate how professional commodity analysts turn raw market data into tradeable insight.

CrudeQ applies the same data sources, signal frameworks, and risk discipline used by institutional energy desks — published weekly, tracked with full transparency. Every call is logged. Every assumption is documented.

Platform Preview

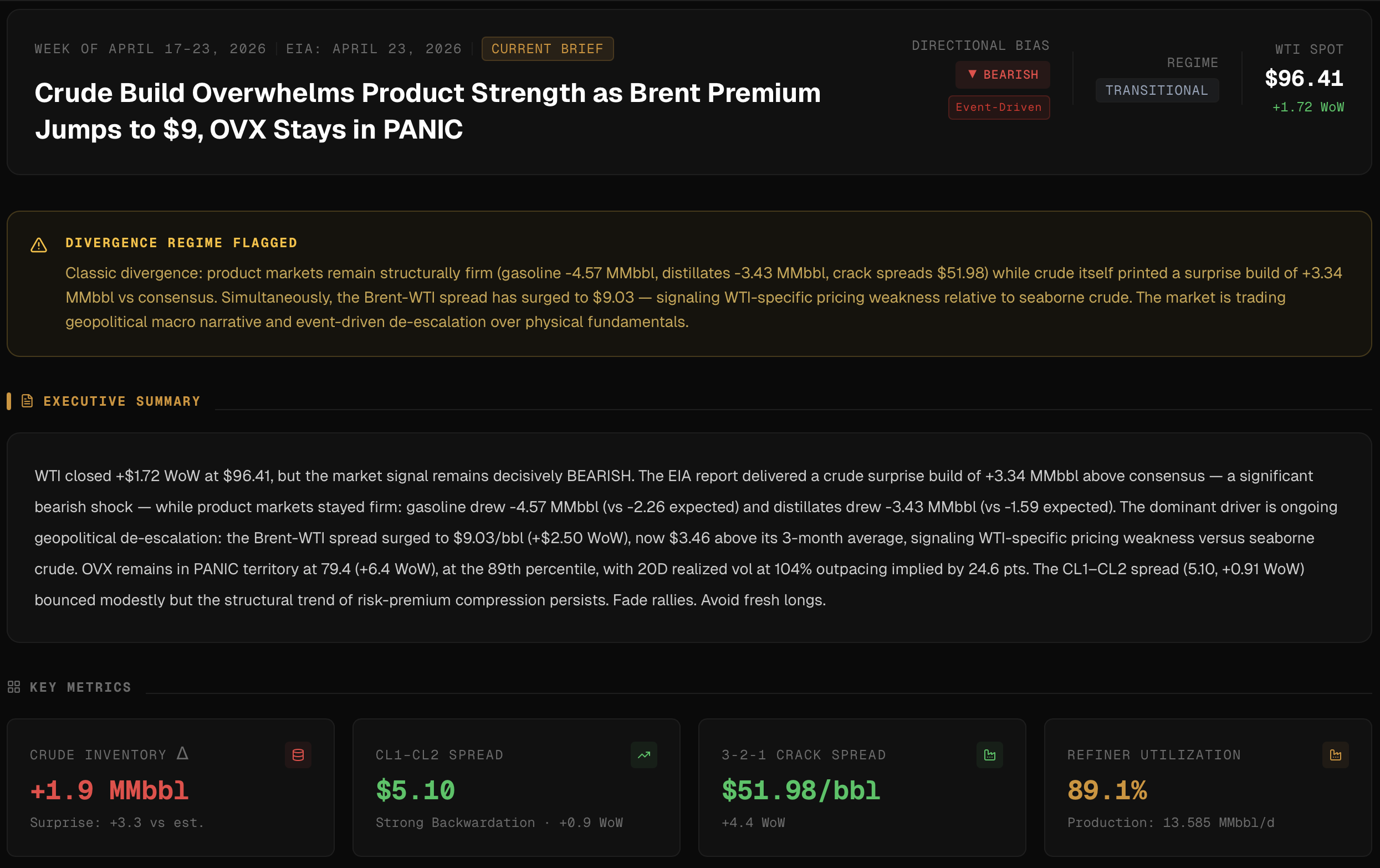

Weekly Brief

EIA signals, regime classification, and directional bias

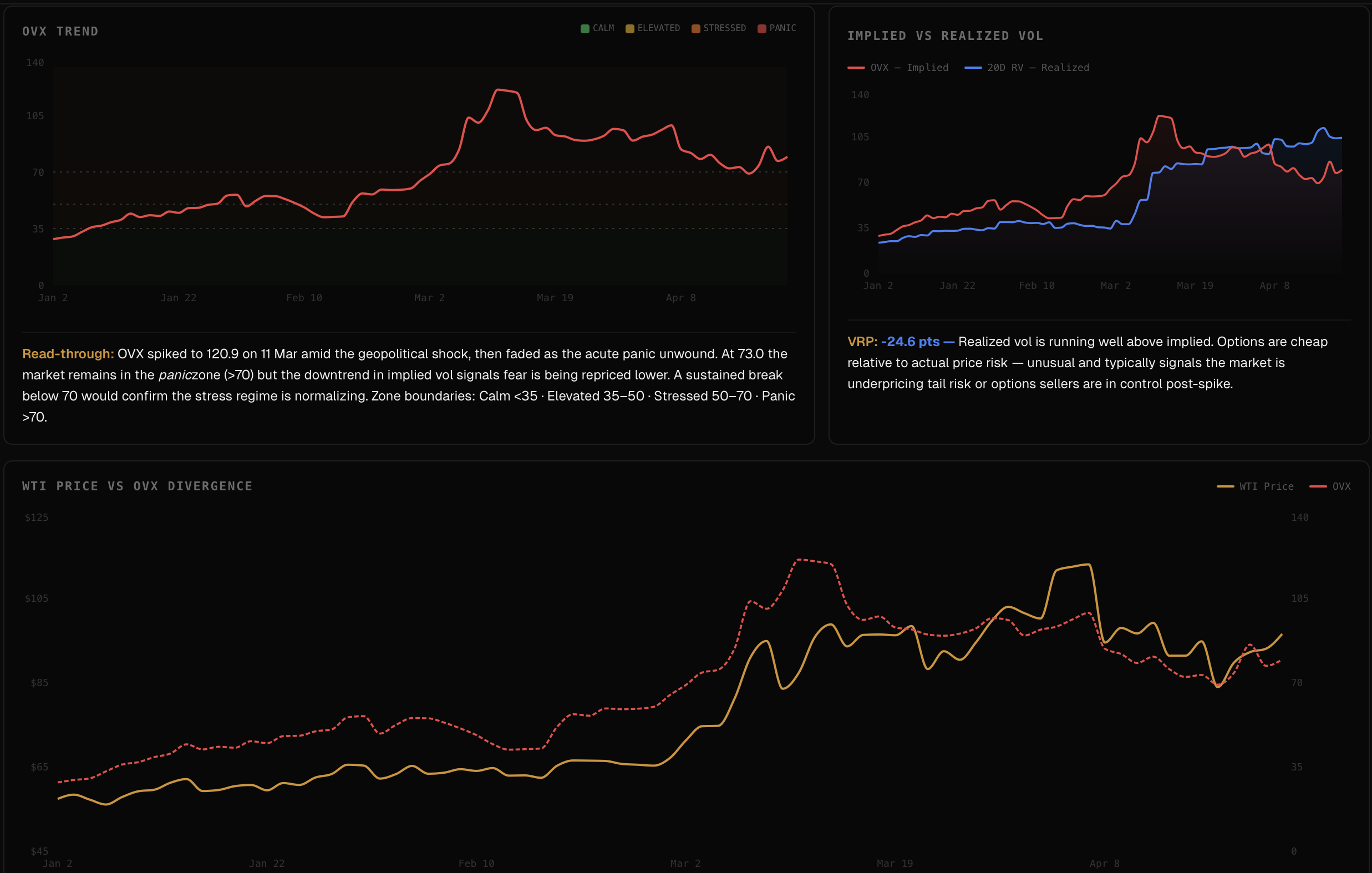

Signal Dashboard

Curve structure, crack spreads & volatility monitor

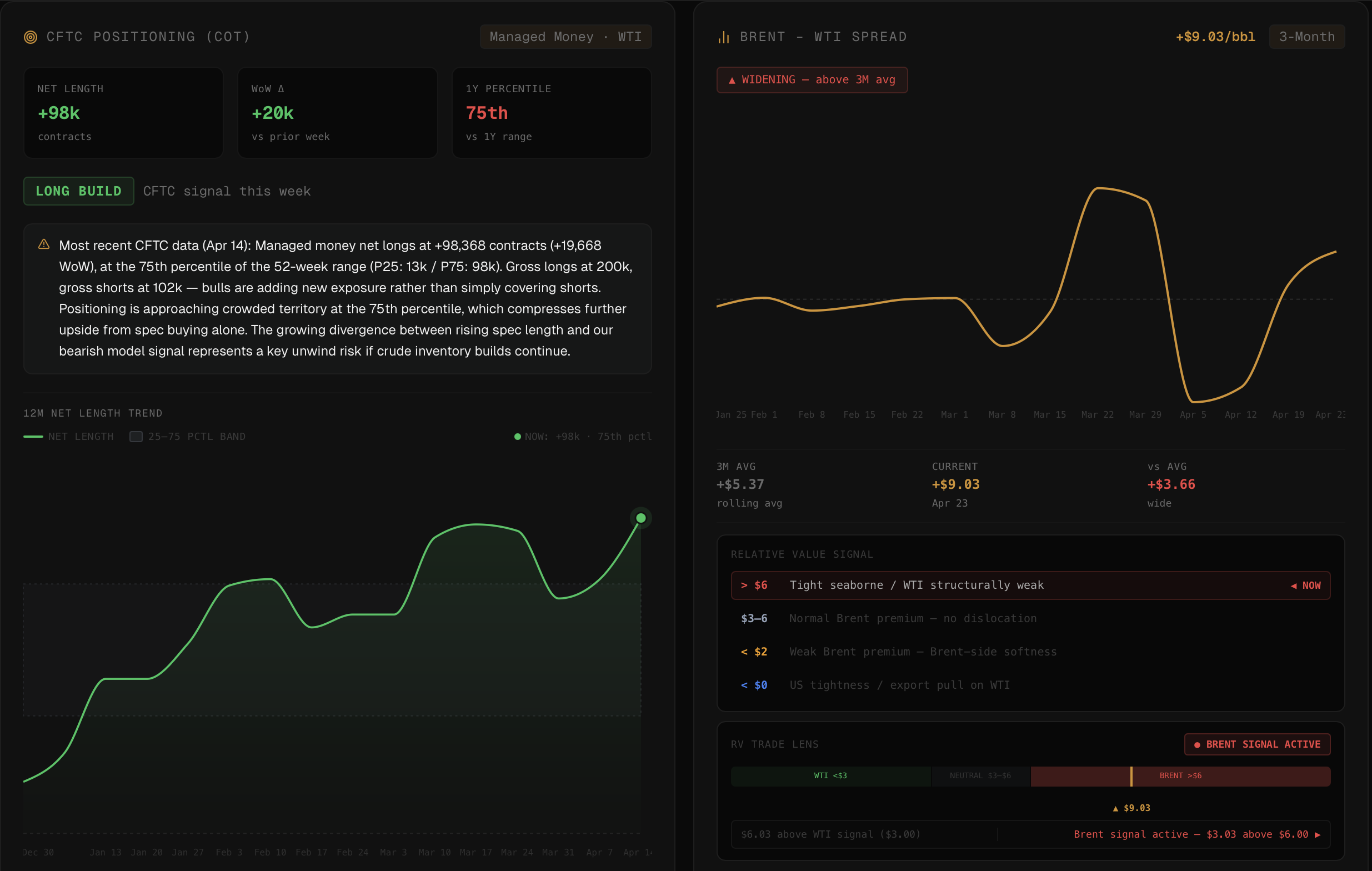

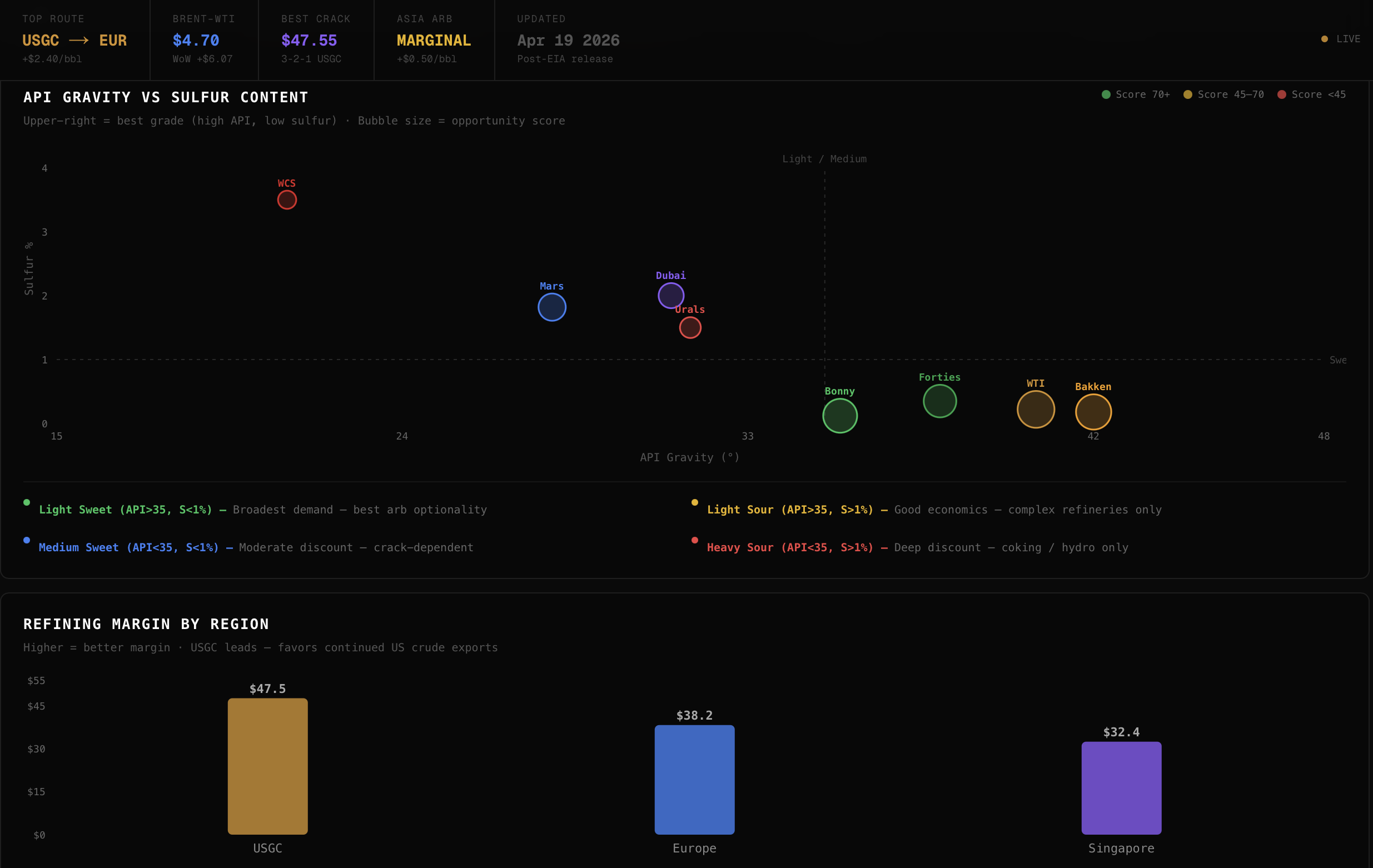

Brent–WTI Spread

Benchmark differential, grade dislocations, and export dynamics

Performance Tracker

R-based equity curve and open position cards

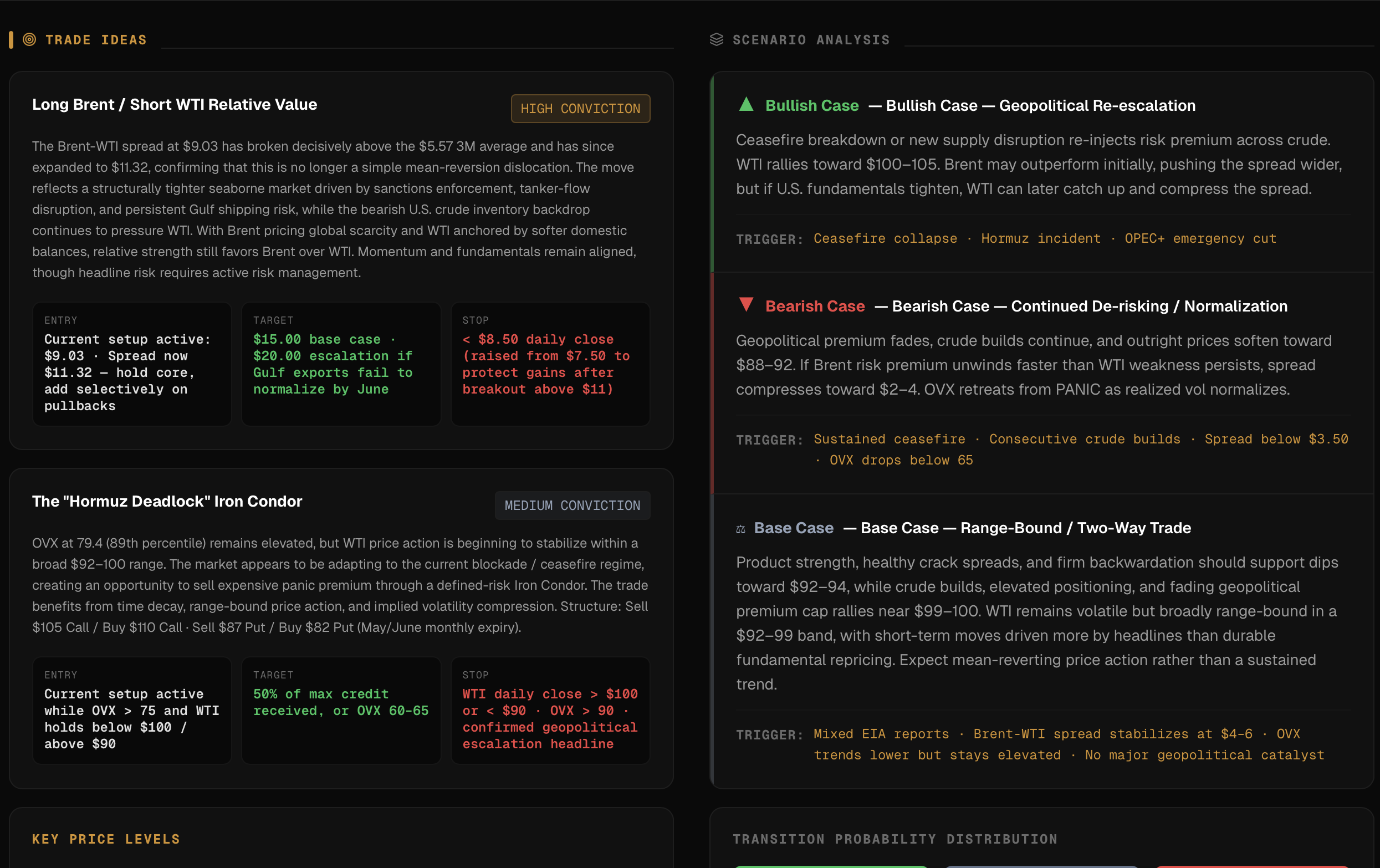

Trade Framework

Entry, target, stop and conviction-weighted sizing

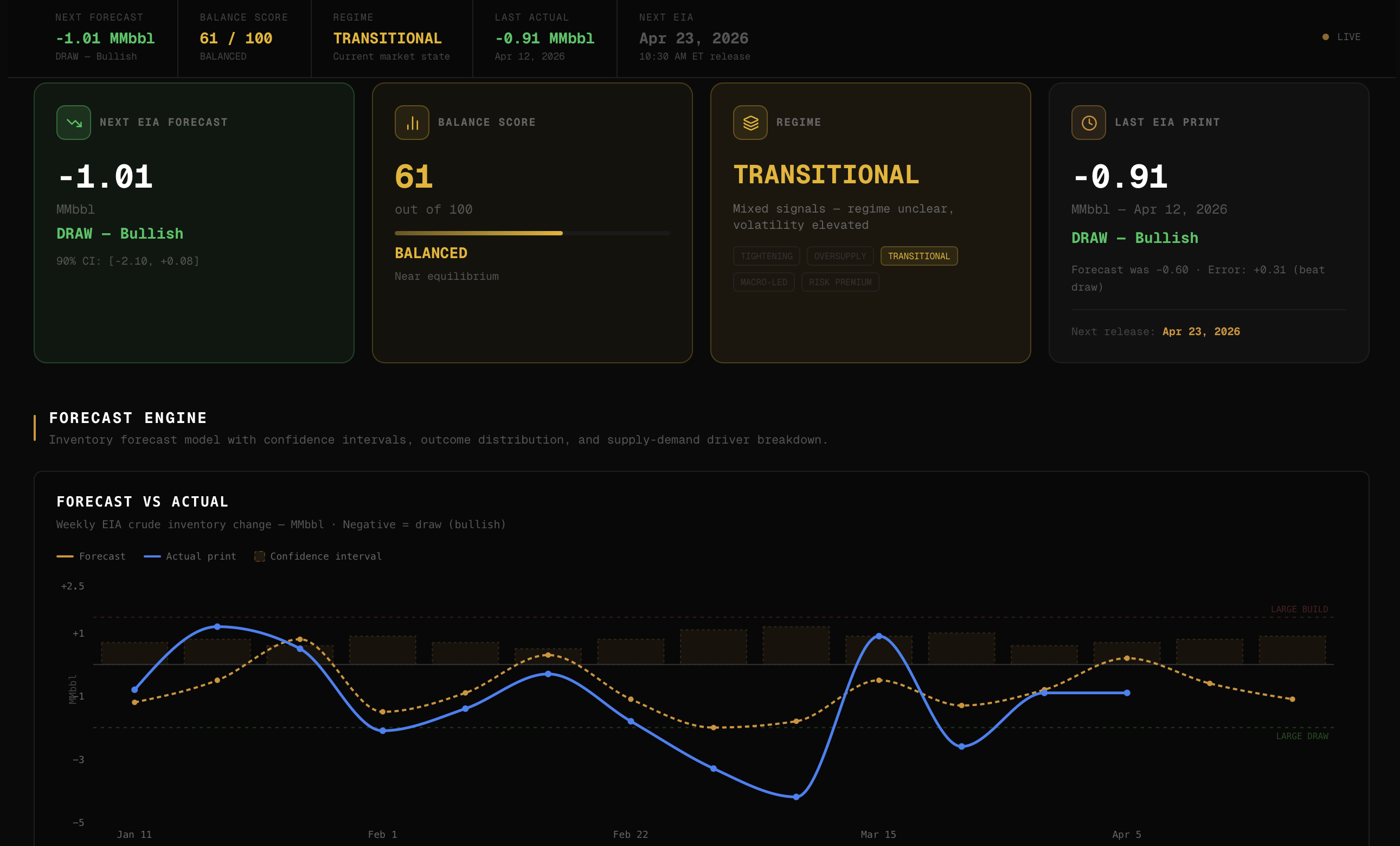

Forecast Beta

Inventory build/draw estimates before EIA release

Arb Beta

Physical route economics and benchmark spread analysis

Why It's Different

Current Publication

Explore This Week's

Market View

May 8, 2026 — WTI Slides 6.4% to $95.42 as Presidential Rhetoric Deflates Value — Massive Bullish EIA Sweep Artificially Overridden by Geopolitics